One of the most frustrating aspects of filmmaking can be financial waste: Paying full license for software you'll only use once. Buying a powerful computer that sits for the 8 hours a day you sleep. Paying for insurance for equipment that sits in the closet 4 days a week. While you can rent software for a single project, or use your overnight time for rendering, insurance has been trickier nut to crack. For drone operators, there is Verifly, an hourly insurance rental app for recreational and commercial drone insurance, backed by Global Aerospace.

Insurance is usually priced to balance out between the relatively safe users and the more reckless ones. However, when I pay for camera insurance, I'm not paying a rate based on a detailed evaluation of how I have treated equipment in the past or the content of the shoot. Unless I've filed an insurance claim in the past, there is no profiling of me as a user, and unless I check off the "working with fire" box, there isn't a huge evaluation of what I'm doing with the gear. Even if I'm doing a stage-bound product shoot, I'm paying an insurance rate that equally covers someone doing crazy reckless things with the camera. It can be frustrating to be paying more to cover for reckless users if you—like me—are one of the exceptionally careful ones, for whom insurance is intended as a back-up.

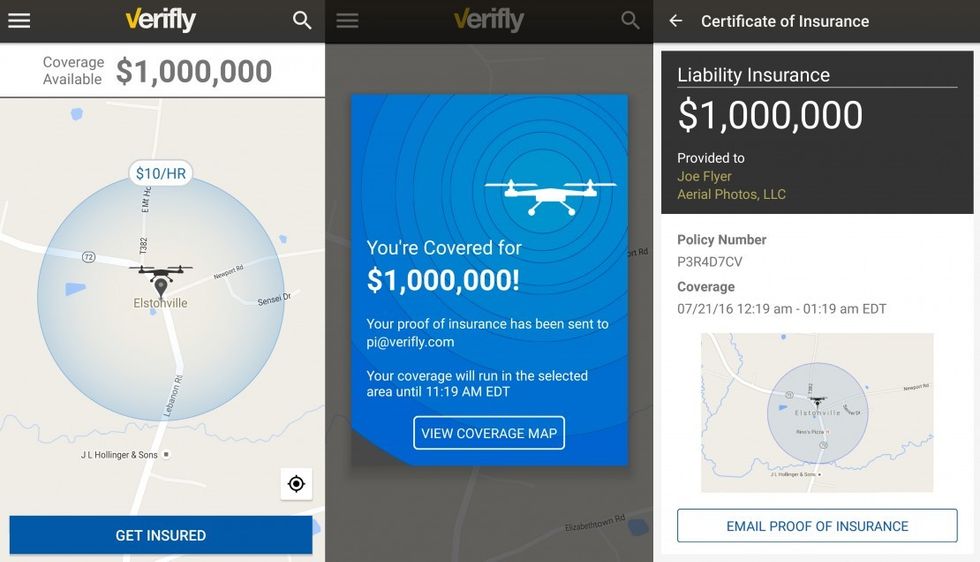

Verifly ScreensCredit: Verifly

Verifly ScreensCredit: Verifly

Some drone operators who would never take their copter up with even a drop of rain in the sky. There are others who will fly their copter anytime they can, up to and including on top of wildfires. Verifly uses data from its app to adjust its pricing based on conditions. Beautiful, windless day? You pay a lower rate. Riskier conditions warrant a higher rate. Right now, it doesn't appear to integrate with the drone operating software, but it is possible to eventually profile users' flying habits and build a user profile to dial in a truly fair insurance price. This is not that different from using an OBD reader to profile drivers for insurance rates.

The biggest upside of this for me comes with freelance drone work. Generally, when doing a gig where bringing along your kit is expected, like a Steadicam or drone shoot, you have to bundle your monthly payments (lease repayment, insurance, maintenance contract),into the price you rent the full package for. It can be hard to nail that pricing exactly. However, with hourly insurance, you can include specific insurance pricing in your bid to client and are able to pass on the price to them. For instance, including a line-item with the insurance estimate—then only charging them for what you end up paying for—is a great way to make sure that your costs are properly being covered by the jobs you do. If you end up shooting for 14 windy hours, and the insurance rate goes up, you can more easily pass that price on, while helping the client understand why that costs more.

I, for one, am excited to see this change in insurance, and I'm looking forward to systems that allow for similar services beyond drones.