A few years ago, it seemed like everything was moving to the blockchain.

Big Hollywood studios are trying to use the Blockchain and related technologies to disrupt the industry. Iced tea chains were adding Blockchain to their name, and even Kodak got in on it, leading to an April's Fools day post of ours which appreciated the fact that Fuji was smart enough to stay above all that nonsense.

But several years later, it's all still here, and continuing to grow, so we wanted to spend a little time on an explainer for how all of this works at the tech level to help folks understand what is going on and how filmmakers might benefit.

What Is the Blockchain?

https://www.reddit.com/r/BrandNewSentence/comments/g5n3r9/imagine_if_keeping_your_car_idling_247_produced/

Many of you might have seen the above meme explaining blockchain, and it's actually not that far from the truth.

Bitcoin, the most famous cryptocurrency, and all other cryptocurrencies, are just one implementation of a technology called blockchain, and it's blockchain more than anything else that might actually be interesting.

But what is it? Is it just solving Sudokus to buy heroin?

Maybe.

The blockchain is a tech that sets out to solve the problem of trust. Most transactions involve trust. You put your money in a bank, you trust that the bank will let you have your money back. That money itself is in a currency usually backed by a government, such as the U.S. government. You trust your bank, and you trust your government, so it works.

What the blockchain is all about is, what if you didn't trust your bank and the government?

https://imgur.com/kvrpjnh

Distributed Ledgers

Blockchain is a technology for a distributed ledger. Instead of a ledger kept in a single place (like a bank), the distributed ledger is kept in many, many places. This idea has been around for a while in low-trust environments like prisons, where multiple ledgers were kept for prison banking physically by hand and they were regularly checked up against each other since no one trusted one individual to honestly keep a record of debts and payments.

The distributed ledger of blockchain is massive. Every single "mining" machine (more on this later) is keeping a seperate copy of the blockchain, and they are all constantly checking them against each other to make sure they are correct.

Every single transaction is another link in a long chain, one connected to the next, so you can't go back and change any earlier records since it'll break the whole chain. This is super duper cool, if you think about it.

The more machines running the ledger, the more "trustworthy" it is, since there are more copies of the ledger you would need to edit in order to fake anything. With enough machines running the ledger, it becomes functionally impossible to commit fraud.

You need to incentivize people to run those ledgers, so they created "mining."

This means you leave your computer running, and running the ledger. You also have that computer do complicated math equations to "prove your work," and random folks who solve those equations will "win" digital currency that will incentivize them to do the work. You can't just implore them to run the ledger for the glory of the Blockchain Union.

https://imgur.com/VJKhkez

Here is where we get to the "your motor is running" part of the meme.

To mine currency like Bitcoin, you need massive computer setups that burn up a lot of power, which is mostly still made with fossil fuels, though work is going to build mining operations powered by geothermal energy and other forms of renewable energy.

There are actually a lot of different blockchains running. Bitcoin runs on a blockchain (or actually several, since they fork over time as developers disagree on things), and competitors like Doge and Ethereum run their own blockchains. They all offer incentives to users to run the ledger in various ways and are all working to solve different problems for efficient public trust.

NFTs

So that brings us to the newest technology a filmmaker should understand, the NFT. We've got a meme for that as well.

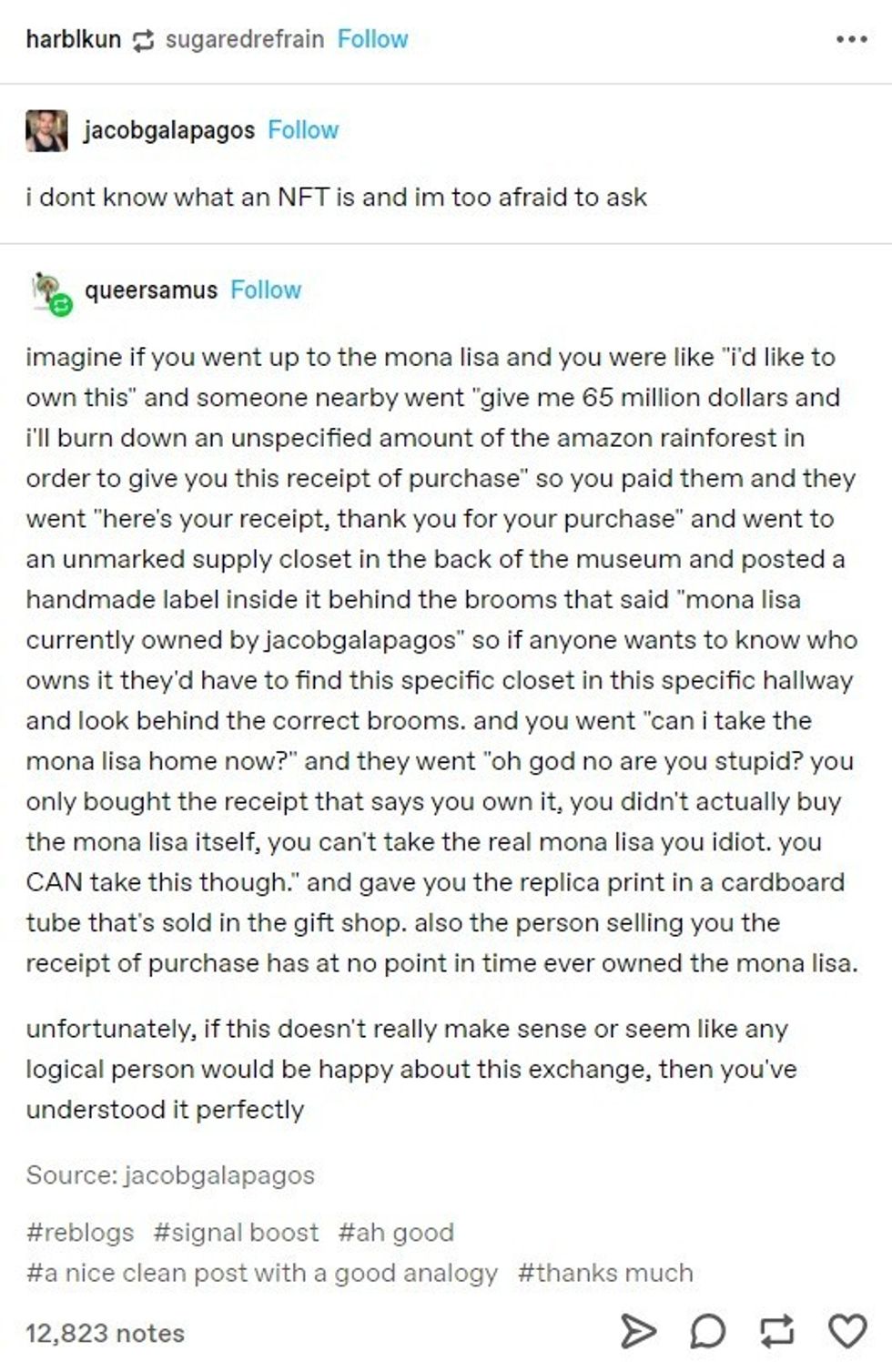

An NFT is a non-fungible token.

Not helpful? Well, basically, it's a receipt that says "you own this" and then points to a digital resource on a server.

Let's say you put a cool photo up on a server. You can sell an NFT saying to someone, "You own that image." However, you only own that image in the world of whatever distributed ledger that NFT runs on (be it Bitcoin or Ether or Doge or whatnot).

It doesn't apply to traditional copyright; folks don't have to contact you to publish the image in a book, they have to contact the original creator or whoever bought the copyright, not the NFT.

If the original server goes down? Tough cookies, kid. The NFT just points to that server, and that server alone. The NFT points to an item and says, "I own that," but that is about it.

There might be potentially cool applications for NFTs, but right now it's seeming like more of a grift than anything else, since most of the major NFT headline sales you hear about are one NFT speculator buying from another to try and drive prices up in the overall market.

We love any idea that allows digital creators to make money, but when comparing things like Patreon to NFT tech, we think Patreon and Kickstarter and Indiegogo were much better innovations for getting money to creators.

Environmental Issues

The other thing that has to be addressed is the carbon footprint of it all. As we watch climate change have dramatic impacts on our current weather systems, with drought, wildfire and flooding becoming constant companions, we need to look at every possible solution to bring down our carbon emissions and prevent catastrophe.

Bitcoin, just one cryptocurrency running on one blockchain, is using up more electricity than all of Argentina. Which is absolutely bonkers if you think about it.

There are other blockchain technologies like Ethereum that use less power, but Bitcoin remains the most popular platform by far, and that is unlikely to change in the future.

Could It Work for Filmmakers?

Maybe?

The big arguments listed in this article by my distinguished colleague Jason Hellerman give one model, where filmmakers sell NFTs or tokens to a film before it's made as a method for financing a project that otherwise couldn't get financed.

That has some potential utility, so we should absolutely consider it. But the problem is the same one of abundance; there are tens of thousands of cryptocurrencies competing for attention, and only a few Bitcoin and Dogecoin winners.

If you are already very famous with a huge following of supporters, you could launch a coin to fund a project, but you could also just, you know, do a Kickstarter like Zach Braff and Spike Lee have. Simpler, more direct support from your audience for your projects.

But if you are an indie filmmaker working on growing your audience and finding your people, it remains to be seen if the blockchain is going to help you get a film made, and more importantly help that film find an audience. If you were one of the first investors in Bitcoin back in the early 2010s, you could've made money in the platform that you could use to make and market your projects.

But as so often happens, after the "rush," the opportunities dwindle. We keep hearing pitches for platforms to use cryptocurrency or the blockchain to incentivize new creation, but they all feel a bit like a solution in search of a problem. You can launch NFTs or a coin to support your project, but it only works if a lot of people buy into its usefulness, and that only works if you can build a big following.

Which feels less "disruptive" and allowing for new voices and more "another method for those with established followings to create things."

Film finance absolutely needs a revolution, but the jury is still out if blockchain will be it. What do you think?