Have you been freaking out about having lost a ton of income you were counting on in the next few months? You’re not alone. As independent contractors with a sudden devastating pandemic and a small chance for unemployment, the future looked murky. But now we can not only get lost income for ourselves but generate income for others!

Like the proverbial restocking of jumbo toilet paper rolls, the Coronavirus Aid, Relief, and Economic Security Act promises the goods just before we run out. We break it down for filmmakers so you can apply for benefits, and fast.

The CARES Act means two things for filmmakers, editors, DPs, writers, producers, and more:

- unemployment eligibility for independent contractors;

- loans you don't have to pay back for freelancers, small production companies, and all small businesses to stay afloat.

Why the CARES Act is time-sensitive

June 30th is the deadline to apply for the loans, and the sooner you can apply, the better. (I’m not trying to create a panicked rush to the Small Business Association, but now we all know what happens when TP gets sparse, let alone dollar bills for small businesses!)

It's our understanding that the application process for loans is only open until the funds run out. Consider that these loans are open to all businesses across the nation. That means every nose-hair trimmer salesman and self-help life coach out there can also apply for these funds.

The process for unemployment is less established right now because the state you live in is likely waiting for clarification from the federal government on when they will be getting the funds from CARES to disperse as unemployment benefits. However, July 31st is the end of the period for which you can get the extra funds under Pandemic Unemployment Assistance. After July 31, you can still get the regular state rate of unemployment, but not the extra $600 a week. So the time is nigh. Read on to understand more.

July 31st is the end of the period for which you can get the extra funds under Pandemic Unemployment Assistance.

Part 1: New unemployment benefits for independent contractors

As we explained before, filmmakers in the time of coronavirus face the usual dilemma: no W2s means no unemployment benefits. And the majority of freelance filmmakers get paid in 1099s. That all changes under CARES Act with the Pandemic Unemployment Assistance program.

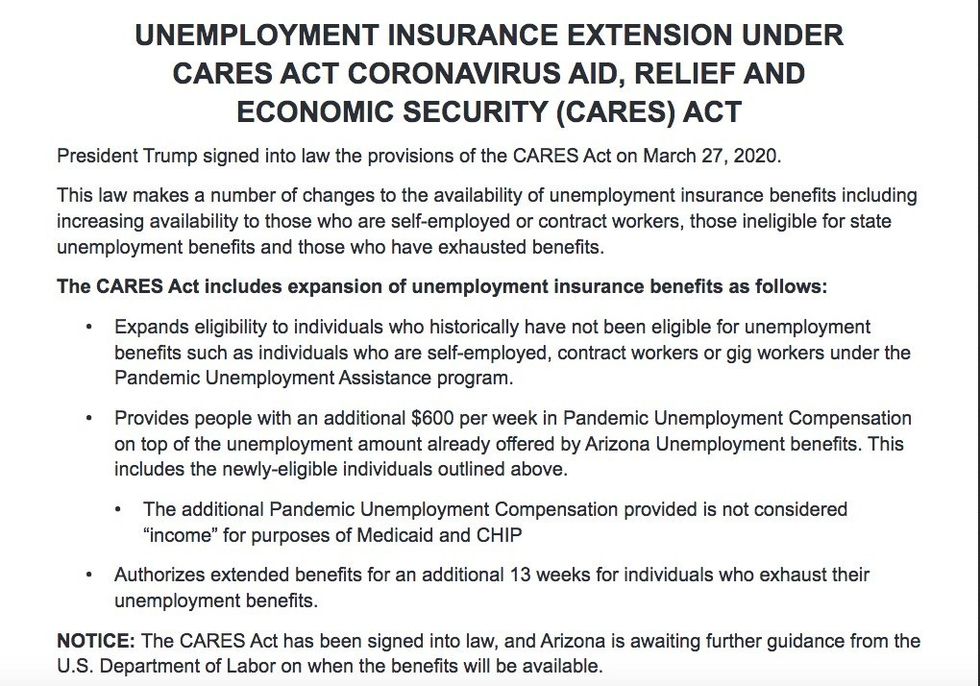

What is Pandemic Unemployment Assistance?

Here’s how it is described by all states, including the Department of Economic Security in my home state of AZ:

How much can you get?

$600 a week in addition to benefits from your state, which tend to be between $200-$300 a week. So you’re looking at $800-$900 a week if you get the max, until July 31. Why July 31? It just happens to be what they wrote in the CARES Act. However, you are not cut off after that. The regular state unemployment has been extended for 39 weeks (about 10 months). In the past, the amount your receive from unemployment was based on your prior income; we do not yet know if that is the case here. For example, if you only made $300 before, will you be eligible for $900 a week now? Probably not, but we will update when we find out for sure. You can re-read How Filmmakers Can Recover Lost Income During COVID-19 for a primer on unemployment benefits.

Who is eligible?

If you are an independent contractor who lost income from coronavirus, you are eligible! Here is the description from CareerOneStop, a partner site of the Department of Labor:

"In March 2020, new federal law greatly expanded unemployment insurance. Many workers who were not previously covered are now eligible. You may now be eligible if any of the following are true:

• Your employer permanently or temporarily laid you off due to coronavirus measures

• Your employer reduced your work hours due to coronavirus measures

• You are self-employed and have lost income due to coronavirus measures

• You’re quarantined and can’t work due to coronavirus

• You’re unable to work due to a risk of exposure to coronavirus

• You can’t work because you’re caring for a family member due to coronavirus"

How to apply?

Select your state on CareerOneStop here. It will lead you to information from your state and how to apply or begin your claim. Should you apply now? We think so.

For example, the AZ Department of Economic Security goes on to say that freelancers should apply now:

“For those who are self-employed, independent contractors, nonprofit employees, and gig economy workers, or requesting an extension of benefits and are not currently filing weekly claims, please submit your initial application now.”

Note that Arizona, like every state, is still “awaiting further guidance” from the Department of Labor. In other words, they aren’t giving out anything yet. But applications are welcome.

If you are an independent contractor who lost income from coronavirus, you are eligible!

What does this mean for the future?

And here’s an interesting prognostication from CNBC on how this could affect freelancers in the future for the better:

"Once the crisis passes, some experts on the freelance economy believe the bipartisan support for providing unemployment to freelancers could signal a new era for independent workers — one in which the idea of providing a government safety net to people outside of traditional jobs goes more mainstream."

Fingers crossed.

Part 2: Loans (that don't have to be repaid)

There are two kinds of loans spelled out for small businesses in the CARES Act that can apply to small businesses or sole proprietorships like production companies.

"...the bipartisan support for providing unemployment to freelancers could signal a new era for independent workers..."

Payroll Protection Plan

Here’s what we know from the COVID-19 Emergency Loans: Small Business Guide:

"The Coronavirus Aid, Relief, and Economic Security (CARES) Act allocated almost $350 billion to help small businesses keep workers employed amid the pandemic and economic downturn. Known as the Paycheck Protection Program, the initiative provides 100% federally guaranteed loans to small businesses. Importantly, these loans may be forgiven if borrowers maintain their payrolls during the crisis or restore their payrolls afterward. The U.S. Chamber of Commerce has issued this cheat sheet to help small businesses and self-employed individuals prepare to file for a loan.

Who is eligible?

- A small business with fewer than 500 employees

- A small business that otherwise meets the SBA’s size standard

- A 501(c)(3) with fewer than 500 employees

- An individual who operates as a sole proprietor

- An individual who operates as an independent contractor

- An individual who is self-employed who regularly carries on any trade or business

- A Tribal business concern that meets the SBA size standard

- A 501(c)(19) Veterans Organization that meets the SBA size standard

What do you mean, you don't have to pay back the loan?

According to the CARES Act, borrowers are eligible to have their loans forgiven. Here’s the official description from the SBA:

"The loan will be fully forgiven if the funds are used for payroll costs, interest on mortgages, rent, and utilities (due to likely high subscription, at least 75% of the forgiven amount must have been used for payroll). Loan payments will also be deferred for six months. No collateral or personal guarantees are required. Neither the government nor lenders will charge small businesses any fees.

Forgiveness is based on the employer maintaining or quickly rehiring employees and maintaining salary levels. Forgiveness will be reduced if full-time headcount declines, or if salaries and wages decrease. This loan has a maturity of 2 years and an interest rate of 1%."

How much?

Evidently you can ask for what you spent on the following items during the 8-week period beginning on the day you get the loan:

- Payroll costs (using the same definition of payroll costs used to determine loan eligibility)

- Interest on the mortgage obligation incurred in the ordinary course of business

- Rent on a leasing agreement

- Payments on utilities (electricity, gas, water, transportation, telephone, or internet)

- For borrowers with tipped employees, additional wages paid to those employees

Find out more info at Small Business Association here.

Economic Injury Disaster Loan

The EIDL is the murkiest to us right now, but also the most promising for filmmakers. Basically, there is an EIDL loan and/or an EIDL Emergency Grant.

The EIDL is a federal disaster loan that has been around for a while. Under the CARES Act, it is expanded and supposedly comes with fewer strings attached. Depending on how much you need, you get it in three days. You don't need to pay it back as long as you're not gambling it away at online casinos! (No, literally, you can't gamble or do porn with it. Sorry, porn production companies!)

And according to the US Chamber of Commerce, there is no obligation to pay back the loan.

What's it for?

According to Benefits.gov, an EIDL provides "financial assistance (based on amount of economic injury) to small businesses or private, non-profit organizations that suffer substantial economic injury as a result of the declared disaster."

This includes an emergency loan or grant. And according to the US Chamber of Commerce, there is no obligation to pay back the loan.

How much is it?

$10,000 for the Emergency Grant that you don't need to pay back if you follow the rules. Up to $25,000 for EIDL grants with no collateral, and up to $200,000 with no personal guarantee. If you have all those things and need more, hell, you can get up to $2Million.

Here’s a description from Forbes:

"The SBA has started taking applications for the EIDL program, ushering in a streamlined application process today. Under the program, applicants are eligible to get a $10,000 advance on a disaster loan that does not have to be paid back if properly applied to operating expenses. The advance is supposed to be delivered within three days. The maximum loan amount is $200,000."

The eligibility requirements are the same as for PPP.

How to apply?

Visit the Small Business Assocation here.

Up next?

The truth is, the landscape is changing every day, so as updates come in, we will share! If you are pursuing Pandemic Unemployment Assistance, PPP, or EIDL, we would love to hear about your experiences. For now, get little more insight and background into how filmmakers can recover lost income. Check back soon for more updates!