The following material is an excerpt from the No Film School How to Make Money as a Cinematographer course.

As we’ve covered extensively here at No Film School over the years, building a career in film and video is tough work. It requires a great deal of perseverance, creative skills, and, at times, straight luck. To “make it” in this industry, you have to be willing to tackle every challenge and stay open to every opportunity.

That’s why, while we fully condone buying new gear that is right for you when possible, we also advise filmmakers not to overspend or overreach with their resources, and focus instead on learning the fundamentals of cinematic storytelling.

With that in mind, we want to offer some tips on how to invest in the right gear by using the right methods. One of the best ways you can extend your career runway is to find ways to supplement your income by making your cameras and gear work for you.

Here’s everything you need to know about making money off your gear, so you can focus on launching your career.

Focus on the art and not the moneyCredit: Gordon Cowie

Focus on the art and not the moneyCredit: Gordon Cowie

Lease vs. Credit Card

One of the first decisions every filmmaker or content creator will need to make when starting off is how to buy their first camera. In reality, many filmmakers end up using credit cards for emergency purchases. You have a gig, you need that certain piece of gear today, and you put it on a credit card.

This is absolutely fine if you pay that card off every month. Using a credit card like a charge card that you have to pay off monthly is a very common tool in the film industry when dealing with cash flow. You can also accumulate points, which is a perk.

Don't spend it all in one place.Credit: Ales Nesetril

Don't spend it all in one place.Credit: Ales Nesetril

What you need to avoid is using a credit card for a major purchase you won’t pay off within that month. You don’t want to put $10,000 on a credit card that will take time to pay off because credit cards typically come with higher interest rates since they are unsecured debt.

Secured debt is tied to an object, like a car payment or a mortgage payment, and the interest rate is lower since the company can always repossess the equipment if you fail to pay. Credit cards are not tied to the item purchased, so you pay higher interest for convenience.

However, there is a secured debt tool we can use, and that is the $1 buyout lease. It’s a lease, meaning the leasing company buys the gear, owns it, and leases it to you. A $1 buyout means if you want to keep it when you are done, it only costs you $1 to do so, and you can keep the camera forever if you like. Because it’s a lease, you can write it off your taxes without worrying about depreciation, and you get to spread your payments out over the equipment's usable life.

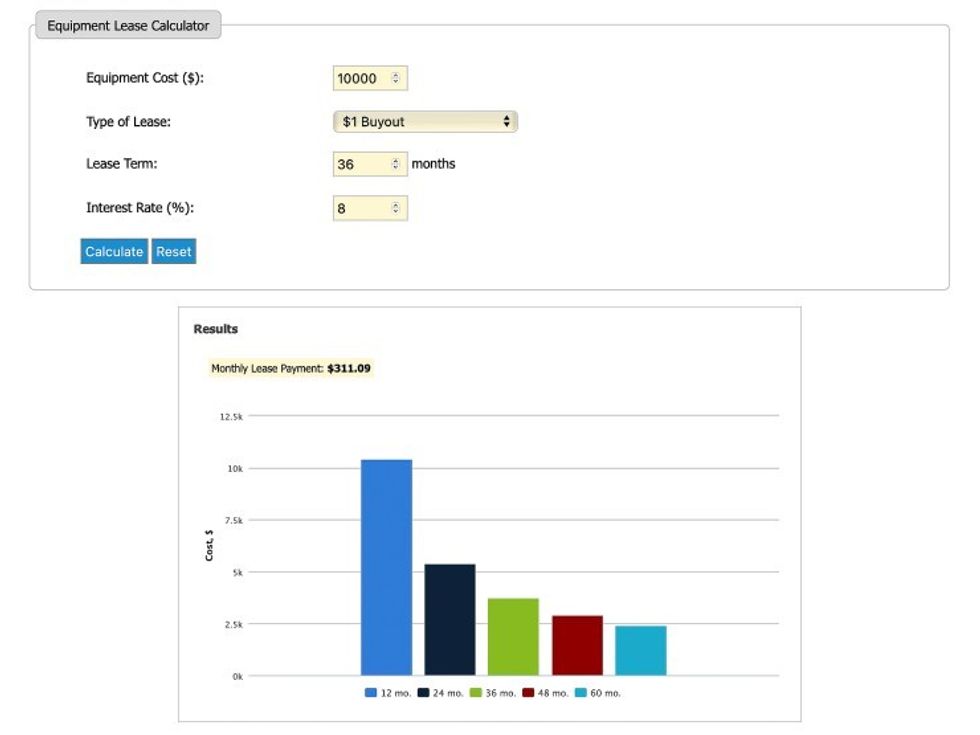

Also, because it’s secured, interest rates are much lower. It’s very common to get under 10%, and you can find interest rates ever lower than that when the prime rate is low. Let’s look at a repayment plan for a $10,000 secured equipment purchase (say, a camera) over 36 months.

Sample Equipment PurchaseCredit: Good Calculators

Sample Equipment PurchaseCredit: Good Calculators

So, with that plan, you pay $311.09/month for 36 months, and you are clear on the equipment purchase. Pay $1, and keep the camera forever at that point. Your total cost is $11,199.24. You’ve paid nearly $2,000 in interest and fees, but as we discuss in our lease resource, you’ve likely saved that amount or more in taxes, and you have cash on hand for emergencies, so it’s worth it in the long run.

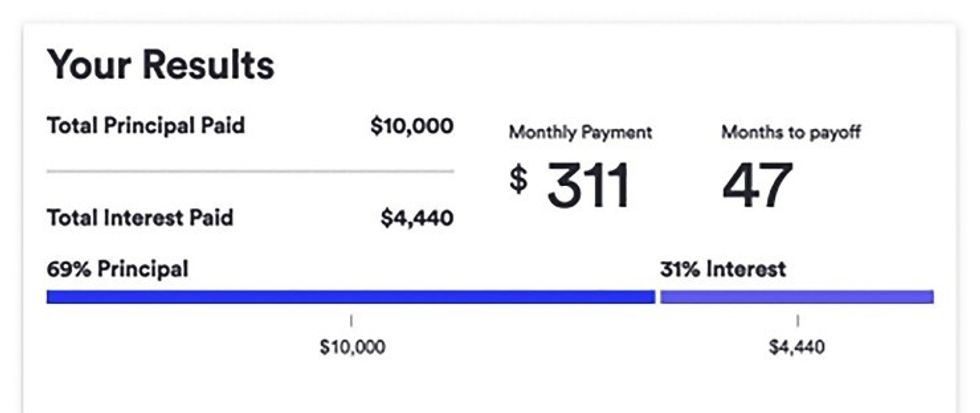

By comparison, if you put that same $10,000 purchase on a credit card, this is how long it takes to repay:

It takes 47 months. That’s a full 11 months longer to repay, still making that same $311/month payment. You might have gotten points that are maybe worth $100 or so in airfare, but then you are paying an extra $3,000 in interest over those last 11 payments.

Hopefully, this will help you always remember that you should consider not putting a major equipment purchase on a credit card. It’s always worth it to consider pursuing a lease for anything you can secure. Credit cards are for emergencies and short-term cash flow issues you’ll pay off immediately, but they may not be the right fit for buying a camera.

Depreciation and Leases

Moving on, let’s dive into talking about why it makes more sense to pay off your gear over time than it does to pay it off all at once.

For reference, we’re going to say that this is a $10,000 investment in gear. That could be building a new color suite with the best monitor or bulking up your lighting package, but for most of us, that’s going to be cameras, lenses, and support. We choose $10,000 to make your math easy.

Let’s say this is a Blackmagic 12K and a tripod and a sigma cine zoom—a pretty basic but versatile package.

Blackmagic URSA 12KCredit: Blackmagic Design

Blackmagic URSA 12KCredit: Blackmagic Design

Before we get to depreciation, let’s talk about another key concept first—cash on hand.

If you have $10,000 in the bank and you buy a $10,000 camera, you now have $0 in the bank. So, if a client is late to pay you on an outstanding invoice or your favorite light breaks and you need a replacement, you are out of luck. Stuck. Busted. Flint. Out of cash.

But if you have $10,000 in the bank and you finance your new camera, then you are still likely have $8,500 or so (after the downpayment) in the bank. So, if a client is late, or you need that new light, you have cash on hand to cover the unexpected. That’s a major benefit. Cash on hand is vital for surviving this freelance business.

Beyond even the benefit of cash on hand, however, there is another major perk to purchases. Depreciation of your gear over time affects your taxes.

Here is the key. For major equipment purchases, you have to depreciate the value of the write-off. This means that if you make $10,000 in a given year and you spend that $10,000 on equipment, you shouldn’t write off that $10,000 on that given tax year’s taxes. You only write off a certain amount and spread the rest over the years of usable life the equipment has.

You can't write everything offCredit: Kelly Sikkema

You can't write everything offCredit: Kelly Sikkema

To keep it simple, let’s say you are expecting five years of usable life on that gear. Instead, you can write $2,000 off on your taxes each year for 5 years. You should also not write off the resale value of the gear, but the value of a five-year-old camera that's lost its “heat” and isn’t going to resale for much. This way, we don’t have to worry as much as we do about a property or a car, as those will have more resale value after five years.

If you pay cash for a camera package, then you must make $10,000 in income to pay for the camera. In our dream scenario, you could buy a camera for $10,000, write that camera off against the income, and save yourself any tax burden for that $10,000 income! Hooray—you might be thinking.

However, the truth is that because the gear you bought has a usable life over time, that is part of how you write it off. You are going to be taxed on $8,000 in income because you can only write off $2,000 of the purchase the year you bought it. Assuming a 30% tax rate, you will pay an extra $2,400 in taxes the first year you own the camera for the $8,000 in income you made to buy the camera. And worse, you already used that $2,400 to buy a camera, so you need to find it somewhere else in your cash flow.

Now, instead, you lease. You can completely write off a lease on your taxes. Using a lease calculator, like this one from good calculators, we can get a sense of how our lease will work out for us.

That $10,000 camera will run you around $300/month when leasing, depending on interest rates. That’s $3,600 a year. But that is $3,600 that you can fully write off your taxes because it’s a lease payment, not an equipment purchase. The rest of your $6,400 is still in your bank account, and while you’ll be taxed on it, that tax bill is only $1,920 (so a $480 tax savings), and even better, you’ll have the cash on hand to pay it.

It's all about having cash on handCredit: Alexander Grey

It's all about having cash on handCredit: Alexander Grey

Over the course of the lease, the tax savings generally works out to be worth it compared to outright purchasing the gear and having to write the purchase off over time. Even in times when interest rates are high, and the tax savings match up with the lease costs, it’s still usually a good idea to keep more of your cash in your bank account.

Interest rates are often lower for a lease than they are for other debt since it’s a secured debt. The loan is for a specific piece of gear that the loan company can repossess and resell in the case of a default, which makes it safer for the lender. This means that your gear will always be much cheaper through a lease than through something unsecured, like a credit card.

Try to work with a lender that is experienced with motion picture gear purchases since they will be more flexible in understanding the entire package of gear needs you have whenever possible.

Other Ways to Make the Money As A Cinematographer

As you can see, there are numerous advantages to leasing your gear, but what else do you need to know about running your business as a cinematographer?

Well, NFS has created a course to teach you just that! The How to Make Money as a Cinematographer course is a collection of 75 chapters, 8 hours of video lessons, and over 50 written resources that will teach you not the craft, but the business of being a cinematographer.

Our goal is to teach you all the things that you need to level up your career. Learn the proper way to shoot branded content, climb the crew ranks to your dream position, and discover how to find new clients. But that's only a small percentage of what you'll learn!

Here at No Film School, we've always strived to give you the knowledge you need to succeed. Now we have a course that will go more in-depth than we ever have.

Start Building Your Dream Career Today

This resource was made specifically for cinematographers that want to build a business that will — make them money! Start 2023 by leveling up your career with No Film School as your teacher.